Wal-Mart Stores: A high dividend growth company

Submitted by Dividend Growth Investor as part of our contributors program.

Wal-Mart Stores, Inc. (WMT) operates retail stores in various formats worldwide. It operates retail stores, restaurants, discount stores, supermarkets, supercenters, hypermarkets, warehouse clubs, apparel stores, Sam’s Clubs, and neighborhood markets, as well as walmart.com; and samsclub.com. The company is a member of the dividend aristocrats index, has paid dividends since 1973 and increased them for 39 years in a row.

The company’s last dividend increase was in March 2013 when the Board of Directors approved an 18.20% increase to 47 cents/share. The company’s largest competitors include Target (TGT) and Costco (COST)

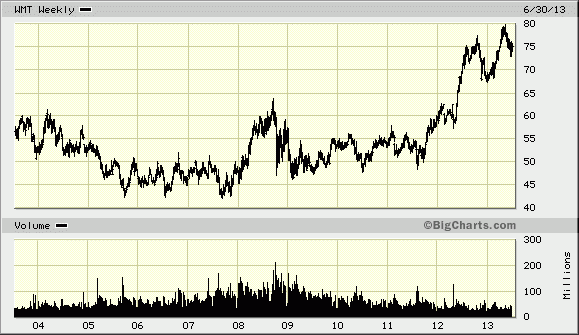

Over the past decade this dividend growth stock has delivered an annualized total return of 5.30% to its shareholders.

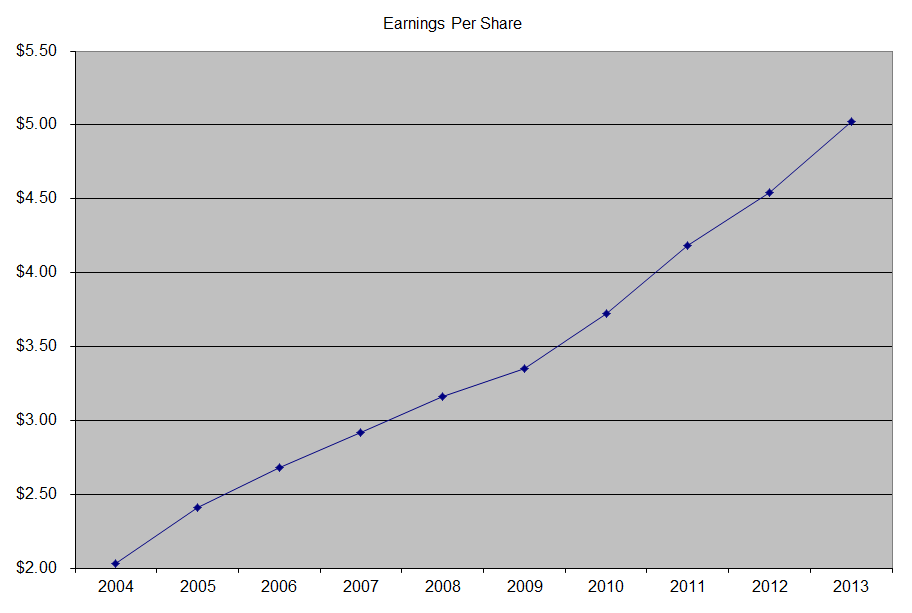

The company has managed to an impressive increase in annual EPS growth since 2004. Earnings per share have risen by 10.60% per year. Analysts expect Wal-Mart Stores to earn $5.30 per share in 2014 and $5.82 per share in 2015. In comparison Wal-Mart Stores earned $5.02/share in 2012. On average, Wal-Mart has also managed to repurchase approximately 4.08% of its shares outstanding each year over the past five years as well.

Wal-Mart has a wide moat, since it is the lowest cost retailer. Its sheer scale gives it a pricing advantage in negotiating with suppliers and its investment in technology allows it to gain further efficiencies across its value chain, thus offering lowest prices in a market. The company has recently refocused in strategy on maximizing return on investment from existing US stores, rather than focusing exclusively on square footage growth. By remodeling stores, and improving their ambiance, it could not only retain its shoppers but even attract different target groups. Its everyday low prices strategy in the US, allows the company to match prices by competitors on items that happen to have lower prices that Wal-Mart. It would take a competitor a considerable investment in a number of stores, distribution centers, technology and logistics in order to emulate Wal-Mart’s business model.

Its international segment however is expected to have low double digit growth in square footage, International currently represents an important opportunity for growth, as it only generates one third of the company’s revenues. Future growth in its international segment could come from acquisitions, as well as organic growth. Wal-Mart is just getting started in certain key markets such as China and India for example. The combination of rising populations, increasing per capita incomes and providing an efficient retailing experience, are some of the characteristics that could fuel growth in international.

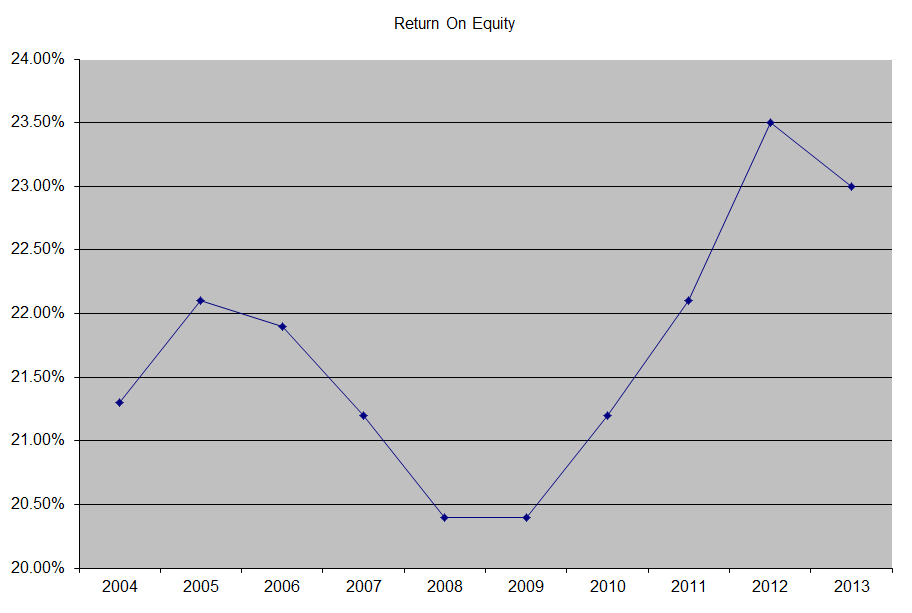

The return on equity has remained consistently above 20%, and has increased to 23% by 2012. Rather than focus on absolute values for this indicator, I generally want to see at least a stable return on equity over time.

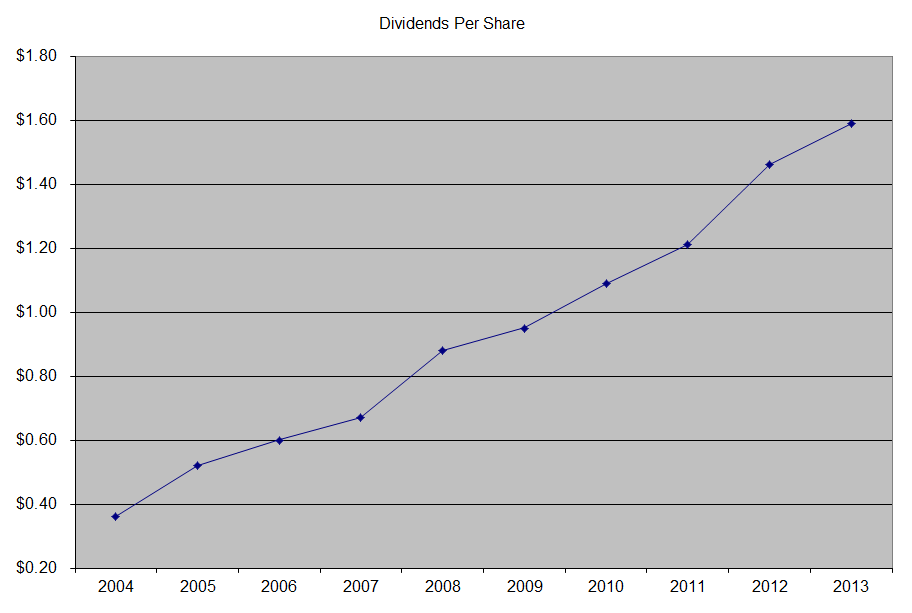

The annual dividend payment has increased by 18.10% per year over the past decade, which is higher than to the growth in EPS.

An 18% growth in distributions translates into the dividend payment doubling every four years. If we look at historical data, going as far back as 1976 we see that Wal-Mart Stores has actually managed to double its dividend every three years on average.

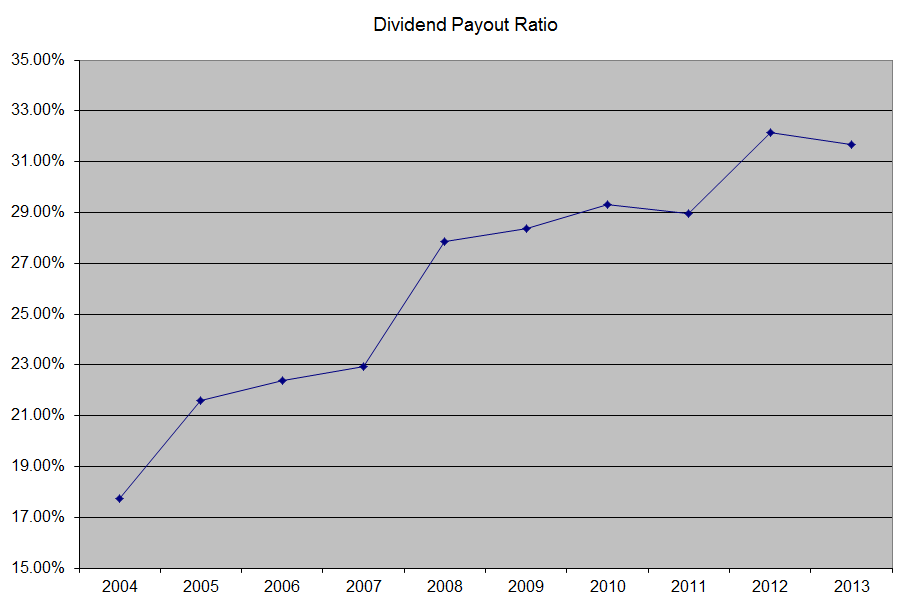

The dividend payout ratio has increased from 17.70% in 2004 to 32% in 2012. The expansion in the payout ratio has enabled dividend growth to be faster than EPS growth over the past decade. A lower payout is always a plus, since it leaves room for consistent dividend growth minimizing the impact of short-term fluctuations in earnings.

Currently, Wal-Mart Stores is attractively valued at 14.30 times earnings and has an adequately covered dividend but only yields 2.50%. In comparison, Target trades at 15.40 times earnings and yields 2.50%.

Disclosure: I am long WMT, TGT. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article.