Barrick Gold: Stock With 30% Upside Potential

Despite rising more than 56% from its March 2020 lows, at the current price of $25 per share, Barrick Gold stock (NYSE: GOLD) is still undervalued and seems like a good bet at the present time. Barrick Gold’s stock has rallied from $16 to $25 off the recent bottom compared to the S&P 500 which increased a little over 65% during the same period. Initially (March to October 2020) GOLD stock outperformed the market due to a sharp rise in gold prices during the current pandemic, which benefited Barrick Gold as 94% of its revenue comes from the yellow metal. However, GOLD’s stock price declined in the last 2 months on the back of a drop in the global gold prices with lockdowns being lifted.

With the gradual lifting of lockdowns and easing of supply constraints, production and shipments are expected to go up in the coming quarters. Additionally, despite recent volatility, the global gold price outlook still remains positive due to expectations of low interest rates, a weak dollar, and demand for physical gold from emerging markets. We believe higher revenue and improved earnings in 2021 along with an elevated P/E multiple is likely to drive another 30% rally in the stock from its current level. Our dashboard What Factors Drove 70% Change In Barrick Gold Stock Between 2017 And Now? provides the key numbers behind our thinking.

- Barrick Vs. Gold: Why The Stock Is Falling Behind

- Higher Gold Prices, Improving Production Will Drive Barrick’s Q2 Results

- Despite Strong Gold Prices, Barrick Stock Is Down 11% This Year. Is It A Good Bet?

- Barrick Stock Trades Below Intrinsic Value Despite Firm Gold Prices And A Strong Production Outlook

- Why Barrick Stock Is Underperforming Despite Strong Gold Prices

- Will Barrick Gold Stock Recover From The Sell Off?

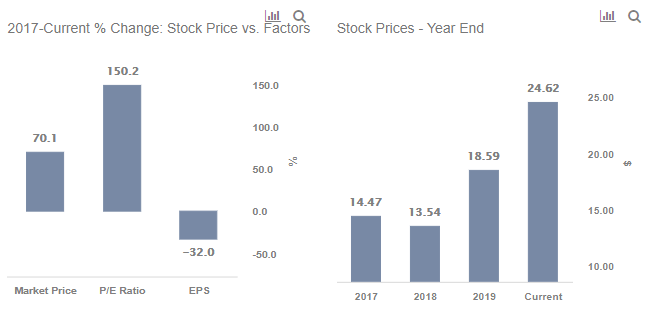

Some of the stock price rise during the 2017-2019 period is justified by the 16% growth in revenues. Barrick Gold revenues increased from $8.4 billion in 2017 to $9.7 billion in 2019, with all the increase coming in 2019, mainly driven by the acquisition of Randgold Resources. This was offset by a 10.7% decrease in profitability as net income margin declined from 10.5% in 2017 to 9.3% in 2019. This decline was mainly because of margins dropping significantly in 2018 on the back of a decline in revenues, lower grade ores, and impairment charges. Margins recovered in 2019 but stayed slightly shy of the 2017 level. On a per share basis, adjusted earnings decreased from $0.75 in 2017 to $0.51 in 2019.

Despite the drop in EPS, the stock price continued to increase due to rise in global gold prices and formation of the Nevada joint venture with Newmont. This led to an increase in the P/E multiple from 19x in 2017 to 37x in 2019. The multiple shot up further this year and currently stands at little less than 50x, as the stock price increased with the further rise in gold prices during the pandemic.

Where is the stock headed?

A slowdown in economic and industrial activities and expectations of a global recession, following the outbreak of coronavirus this year, has increased gold’s value as a hedging instrument, which, in turn, led to a surge in global gold prices. With rising investment in the yellow metal by major central banks and expectations of interest rates declining, gold prices already saw a sharp rise in 2019. This trend was further boosted by the current Covid-19 crisis. This was reflected in the company’s recent results, where Barrick Gold revenues for the first nine months of 2020 increased 36%, while earnings dropped due to one-time gains reported in the previous year period.

With the gradual lifting of lockdowns, the gold rally also seems to have faced impediments after the price increased from $1,500/ounce at the beginning of 2020 to over $1,950/ounce in September 2020. In fact, with economies opening up, the gold price has declined over recent weeks and has remained volatile, with it coming close to $1,850/ounce in December. However, with the new spike in Covid-positive cases and the economic recovery being slower than expected, gold prices have again increased and currently stand at $1,940/ounce. Precious metals’ price outlook remains positive considering weakness in the dollar, continuity of the low interest rate scenario, and expectations of higher physical demand for gold from emerging economies as stimulus measures continue leading to more liquidity infusion. The actual movement in commodity prices and its timing hinge on the broader containment of the coronavirus spread. Our dashboard Trends In U.S. Covid-19 Cases provides an overview of how the pandemic has been spreading in the U.S. and contrasts with trends in Brazil and Russia.

Rising revenue and margins during the current crisis in 2020, when most industries were adversely affected, is a big positive for the mining giant. Additionally, expectations of continued healthy revenue and margin growth in 2021 due to the Nevada JV (with Newmont) and higher production, and with investors’ focus shifting to 2021 numbers, we believe Barrick Gold’s stock is set to rise further. Recovery in copper prices is also a positive signal for the company As revenue and earnings growth remains strong in 2021 due to higher volume and favorable price realization, the P/E multiple will also remain elevated. At the current level, investors have an opportunity to see a potential upside of 30% in Barrick Gold’s stock, which as per Trefis, has a fair value of $32 per share.

What if you’re looking for a more balanced portfolio instead? Here’s a high quality portfolio to beat the market, with over 100% return since 2016, versus 55% for the S&P 500. Comprised of companies with strong revenue growth, healthy profits, lots of cash, and low risk, it has outperformed the broader market year after year, consistently.

See all Trefis Price Estimates and Download Trefis Data here

What’s behind Trefis? See How It’s Powering New Collaboration and What-Ifs For CFOs and Finance Teams | Product, R&D, and Marketing Teams