After A 40% Fall This Year Is Lululemon Stock A Better Pick Over Electronic Arts?

Given its better prospects, we believe Lululemon stock (NASDAQ: LULU) is a better pick than the gaming company Electronics Arts stock (NYSE: EA). Although these companies are from different sectors, we compare them because of their similar characteristics, including a market capitalization of $35-40 billion, and a gross profit of $5.5-6 billion. The decision to invest often comes down to finding the best stocks within the ambit of certain characteristics that suit an investment style. Electronic Arts stock trades at a higher valuation multiple of 4.8x revenues, versus 4.2x for Lululemon. However, the latter has seen superior revenue growth, is more profitable, and has a better financial position. In the sections below, we discuss why we believe that LULU will offer better returns than EA in the next three years. We compare a slew of factors, such as historical revenue growth, stock returns, and valuation, in the sections below.

1. Both Stocks Have Seen Little Change Since Early 2021

EA stock has seen little change, moving slightly from levels of $145 in early January 2021 to around $135 now, while LULU stock moved from $350 to $320 over the same period. This compares with an increase of about 40% for the S&P 500 over this roughly three-year period.

Overall, the performance of EA stock with respect to the index has been lackluster. Returns for the stock were -8% in 2021, -7% in 2022, and 12% in 2023, while returns for LULU stock were 12%, -18%, and 60% over the same years. In comparison, returns for the S&P 500 have been 27% in 2021, -19% in 2022, and 24% in 2023 — indicating that EA underperformed the S&P in 2021 and 2023 and indicating that LULU underperformed the S&P in 2021.

In fact, consistently beating the S&P 500 — in good times and bad — has been difficult over recent years for individual stocks; for heavyweights in the Communication Services sector including GOOG, META, and NFLX, and even for the megacap stars TSLA, MSFT, and AMZN.

In contrast, the Trefis High Quality (HQ) Portfolio, with a collection of 30 stocks, has outperformed the S&P 500 each year over the same period. Why is that? As a group, HQ Portfolio stocks provided better returns with less risk versus the benchmark index; less of a roller-coaster ride, as evident in HQ Portfolio performance metrics.

Given the current uncertain macroeconomic environment with high oil prices and elevated interest rates, could EA and LULU face a similar situation as they did in 2021 and underperform the S&P over the next 12 months — or will they see a strong jump? While we think both stocks will see higher levels, LULU will likely fare better between the two.

2. Lululemon’s Revenue Growth Is Better

Lululemon’s average annual revenue growth of 30.1% over the last three years has been much better than just 10.7% for Electronic Arts. Lululemon’s revenue rose from $4.4 billion in fiscal 2021 (fiscal ends in January) to $9.6 billion in fiscal 2024, while Electronic Arts saw its top line expand from $5.6 billion to $7.6 billion over the same period.

Gaming companies benefited from lockdowns during the pandemic, as gamers spent more time on gaming. However, this trend has now cooled off. Electronic Arts’ recent revenue growth has been driven by its live services offering, primarily for the FIFA franchise. Furthermore, the company has benefited from its acquisitions of Playdemic, Codemasters, Metalhead Software, and Glu Mobile in recent years. However, the revenue growth has been tepid lately owing to a broader decline in gaming demand. The average quarterly playtime has seen a significant 26% fall between 2021 and 2023. [1]

Looking at Lululemon, an athleisure company, has seen its sales rise over the last few years driven by strong demand in the Americas region. This trend has cooled off lately, primarily due to a change in consumer spending trends and rising competition. The company expects 11% to 12% sales growth in the current year. Our Electronic Arts Revenue Comparison and Lululemon Revenue Comparison dashboards provide more insight into the companies’ sales.

3. Lululemon Is More Profitable And Offers Lower Financial Risk

Lululemon’s reported operating margin stood at 22.9% in 2024, compared to 19.3% in 2021, while that for Electronic Arts improved from 18.6% to 20.9% over the same period. The softness in the U.S. market and planned increased spending to grow brand awareness may weigh on Lululemon’s operating profit margin in the near-term.

Looking at financial risk, Lululemon fares better. Its a debt free company, while Electronic Arts has a $1.9 billion debt, with its debt as a percentage of equity standing at 5%. Also, its 32% cash as a percentage of assets is higher than 25% for Electronic Arts implying that Lululemon has a better financial position.

4. The Net of It All

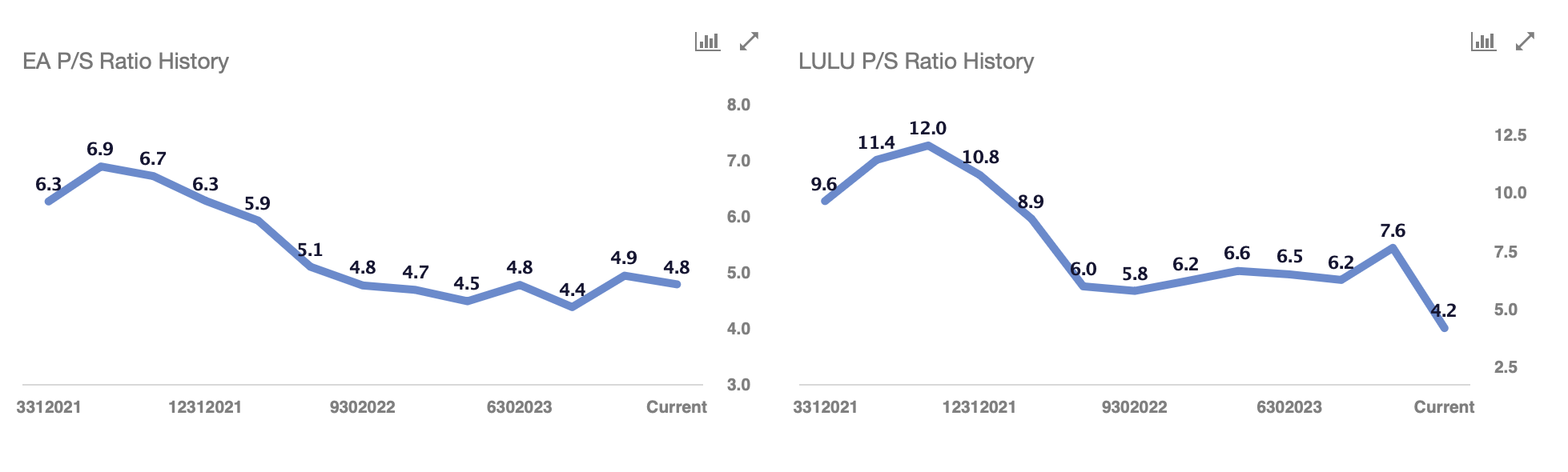

We see that Lululemon has seen better revenue growth, is more profitable, and has a better financial position. Now, looking at prospects, using P/S as a base, due to high fluctuations in P/E and P/EBIT, we believe LULU is the better choice of the two. Let us compare the valuation multiples for both stocks against their historical average. Electronic Arts stock currently trades at 4.8x trailing revenues, vs. the last three-year average of 5.3x. In contrast, Lululemon is trading at 4.2x revenues, lower than its last three-year average of 8.2x. This implies that Lululemon has a better growth potential if the valuation multiples were to return to their historical averages.

Moreover, Lululemon is seeing a pickup in demand for its international business as well. While Electronic Arts may see tepid growth in the near-term owing to a broader decline in gaming demand and fewer titles released, Lululemon is likely to continue to deliver double-digit sales growth. Given that LULU stock has seen a meaningful decline of around 40% this year, its valuation now looks attractive vis-à-vis Electronic Arts, which hasn’t seen any gains this year.

While LULU stock may outperform Electronic Arts in the next three years, it is helpful to see how Electronic Arts’ peers fare on metrics that matter. You will find other valuable comparisons for companies across industries at Peer Comparisons.

| Returns | Jun 2024 MTD [1] |

2024 YTD [1] |

2017-24 Total [2] |

| EA Return | 3% | 0% | 74% |

| LULU Return | 2% | -38% | 389% |

| S&P 500 Return | 1% | 12% | 139% |

| Trefis Reinforced Value Portfolio | 0% | 4% | 641% |

[1] Returns as of 6/10/2024

[2] Cumulative total returns since the end of 2016

Invest with Trefis Market-Beating Portfolios

See all Trefis Price Estimates

- Playtime has decreased since the start of 2021 across the PC and console market, Tom Wijman, Newzoo, April 2, 2024 [↩]