Constant Contact Q2 Earnings Preview: Recovery Expected Post The Change In Brand Positioning

Constant Contact (NASDAQ:CTCT) is slated to release its Q2 2015 results on July 23. The company’s performance in Q1 2015 was below management expectations. Customer additions were less than expected, and was accompanied by a relatively high attrition rate. Constant Contact embarked upon a brand repositioning drive in the first quarter and that backfired. The company tried repositioning itself from an email marketing service provider to an integrated online marketing tool provider. Currently, Constant Contact is trying to revert to its old image. Constant Contact’s performance was also dampened due to a surge of credit card payment failures on its website. For Q2 2015, we expect Constant Contact’s performance to improve over the first quarter, after gaining back the customer confidence with its previous brand image.

Constant Contact’s revenues for Q1 2015 were $90.4 million, reflecting a 14.6% year-on-year rise. The management expected revenues between $90.7 million and $91.3 million. [1] Consequently, Constant Contact has revised its revenue growth expectation for 2015 downwards, from 20% to 12% to 14%, ranging from $371 million to $377 million. ((Constant Contact’s Q1 2015 Earnings Call Transcript, Seeking Alpha, April 30, 2015))

Our $34 price estimate for Constant Contact is around a 10% premium to the current market price.

- Endurance Finalizes Constant Contact Acquisition, Lays Off 15% Of The Staff

- Constant Contact Earnings: Results Were Good Year-On-Year But Fell Short Of Guidance

- Constant Contact Pre-Earnings: Improved Marketing Strategies, Continued Alliances And ‘Galileo’ Could Drive Revenues

- Constant Contact: What Lies Ahead

- Constant Contact Performed Better Than The Previous Quarter, Though Customer Growth Yet To Recover

- The Two Scenarios That Can Impact Constant Contact’s Valuation In Opposite Ways

See our complete coverage of Constant Contact

Single Platform Expected To Fly High

Constant Contact’s Single Platform has historically been a major growth driver and is expected to continue its healthy performance in Q2 2015, as well. Acquired in 2012, SinglePlatform, Constant Contact’s digital listing service, registered over 100% year-on-year top line growth in 2014. Single Platform’s publisher network includes top business directories, search engines, rating and review sites, and mobile discovery applications. Small businesses are benefited by the wide reach and exposure they gain through Single Platform. In 2014, SinglePlatform generated nearly 400 million views for small businesses, displaying an over 20% year-on-year growth in views.

Credit Card Failures Might Continue In Q2 2015

Credit card payment failures have been worsening the company’s customer attrition over the past. The management believed that the issue was settled with the improvement in the credit card acceptance rates towards the end of 2014. However, in Q1 2015, the company again faced the failure of its new credit card processor, and consequently, a higher than planned user attrition. Recent trends reflect that Constant Contact is losing out on 3,500 to 4,000 incremental customers each year, as compared to the previous year due to the credit card failure rates. The cumulative impact of these lost customers over the course of the year is estimated to be around $4 million to $5 million. [2]

The credit card failure trend is expected to continue for the rest of 2015. Unless the management takes some drastic steps to prevent it, Constant Contact’s customer base erosion will continue due to this problem.

Toolkit’s Performance Expected To Recover

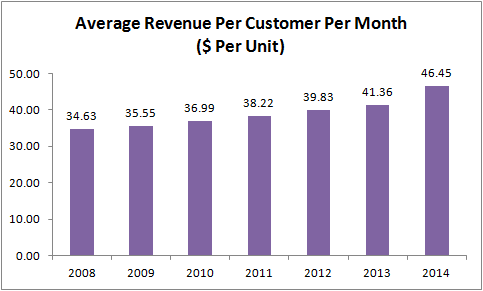

Constant Contact’s integrated marketing suite, Toolkit (introduced in Q1 2014), was a big success in 2014, resulting in ARPU growth of 9% year-on-year to reach $44.94 per user. Toolkit provides an easy way for small businesses and non-profit organizations to launch multiple campaign types across high-return marketing channels, such as email, social, mobile, and Web. This bundled offering has three different packages: basic, essential, and ultimate. However, the beginning of 2015 hasn’t been too positive. The focus on Toolkit and positioning Constant Contact’s brand image as an integrated marketing tool provider, rather than an email service provider, didn’t fare well with users and website visitors. As a result Toolkit’s performance suffered.

In Q1 2015, while the number of visitors to the website was consistent with the management’s expectations, the number of conversions from visitors to free trials fell below expectations. This resulted in a lower number of customer additions. Currently, Constant Contact is striving to go back to its previous brand image through advertisements and messages focusing on its email marketing success to drive users back to its website. [2]

We expect that the company’s efforts will improve the user confidence and, in turn, will grow the adoption rates. As a result, Toolkit’s performance is expected to be better in Q2 2015, as compared to the previous quarter.

The Company Might Be Looking For Takeover Targets

Constant Contact might be on the lookout for acquisitions in 2015. The company’s strong cash position and cash generation (free cash flow of $33 million in 2014 and expected free cash flow for 2015 is $40 million) gives it the capital strength to carry on its plan. However, currently, Constant Contact is focusing on the Canadian and Mexican markets, besides the U.S. According to the management, a wider international expansion is to be expected in 2016-2017 rather than in 2015. [3]

The Domestic U.S. Market Is Expected to Provide Significant Growth Potential

The company has ample scope for growth in the U.S. from where it derives around 90% of its revenues. The driving factors are the improvement in the economic scenario in the U.S. There are more than 31.5 million registered small businesses and non-profits in the U.S., ((Constant Contact Form 10-k, Constant Contact, February 25, 2015)) and hence we believe there is significant scope for the company to expand its customer base and grow its ARPU going forward.

View Interactive Institutional Research (Powered by Trefis):

Global Large Cap | U.S. Mid & Small Cap | European Large & Mid Cap

Notes:- Constant Contact announces Q1 2015 Results, Constant Contact Investor Relations, April 30, 2015 [↩]

- Constant Contact’s Q1 2015 Earnings Call Transcript, Seeking Alpha, April 30, 2015 [↩] [↩]

- Constant Contact’s Q4 2014 Earnings Call Transcript, Seeking Alpha, January 29, 2015 [↩]