Amazon Vs. Alibaba: Cloud Services In Focus

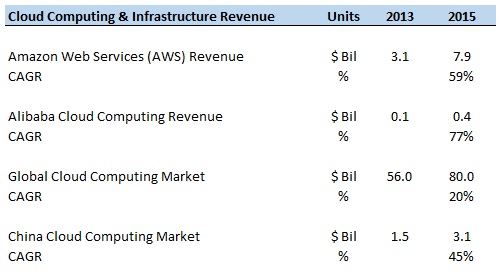

E-commerce giants Amazon (NASDAQ:AMZN) and Alibaba (NYSE:BABA) have both reported massive growth in their cloud computing businesses over the past few years. Alibaba Cloud and Amazon Web Services (AWS) have outpaced the growth in total worldwide spending on cloud computing and infrastructure services. Alibaba has grown at a faster pace than Amazon, primarily due to the fact that it predominantly operates in China, which is a relatively nascent and fast-growing market. In terms of scale, Alibaba’s cloud computing revenues are much lower than Amazon’s AWS revenues, as shown below.

Strong Revenue Growth For Amazon & Alibaba

- Alibaba Stock Is Down 70% From Highs, But Its AI Push Is Yielding Results

- Alibaba’s Q1 Preview: Navigating A Tough Chinese Economy

- What’s Happening With Alibaba Stock?

- Will Alibaba’s Cloud Business See A Turnaround In Q4?

- Down 40% In The Last 12 Months, Is Alibaba Stock Undervalued At $70 Per Share?

- Down 65% Since 2021, What’s Next for Alibaba Stock?

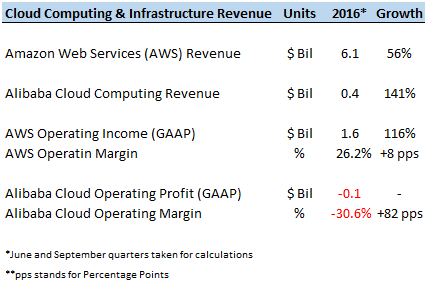

Both Amazon and Alibaba have continued to witness strong growth rates in terms of revenue as well as profit margins in 2016. Amazon reported operating profit margin of 26.2% for its AWS division for Q2’16 and Q3’16 combined, which was almost 8 percentage points higher than the prior year period. Similarly, Alibaba also witnessed a drastic improvement in operating margin in the same period. Although the margin for Alibaba Cloud is still negative, it has shown quarter over quarter improvement through the year. It is likely that Alibaba Cloud could become profitable for the company over the next couple of years.

It should be noted that we have used only June and September quarter figures for comparison since Alibaba just started reporting segment-wise margins in the June quarter last year.

Role of Cloud Business In Driving Company Growth

While both companies are enjoying strong revenue growth in their cloud businesses, there is a huge difference in the contribution of cloud to net profits. Amazon purchases products at wholesale rates and stores the inventory at Amazon Fulfillment Centers and sells them as Amazon Verified Products. This helps in weeding out fake and counterfeit products from its listings – something that Alibaba has reportedly struggled with over the last few quarters. [1] Therefore, Alibaba’s operating profit margin is significantly higher than Amazon’s, since it does not maintain inventory and primarily acts as the aggregator between buyers and sellers. As a result, Amazon’s e-commerce business contributes 92% of net revenues but only a third of the company-wide operating profits. Comparatively, Alibaba’s e-commerce segments combined generate 84% of net revenues and a whopping 169% of operating income.

AWS is effectively helping Amazon expand its e-commerce business in international markets where it is operating at a loss. On the other hand, Alibaba is financing its cloud business and other new ventures such as digital media, entertainment and online video through the profits generated by its core commerce segments.

Robust Long-Term Outlook For Cloud

According to an estimate by Market Research Media, the global cloud computing market is likely to continue to grow at 30% through 2020 to become a $270 billion market similar pace over the next few years. [2] Moreover, the cloud computing market in China could grow at a CAGR of about 45% over the next few years, according to an estimate by Bain & Company. [3] We forecast AWS revenues to grow at almost 30% over the next few years, while Alibaba Cloud revenues could grow at 40% in the same period.

See our full analysis for Alibaba|Amazon.

View Interactive Institutional Research (Powered by Trefis):

Global Large Cap | U.S. Mid & Small Cap | European Large & Mid Cap

More Trefis Research

- Why Alibaba’s Massive Counterfeit Problem Will Never Be Solved, Forbes, November 2015 [↩]

- Global Cloud Computing Market Forecast 2015-2020, Market Research Media, January 2016 [↩]

- Finding the Silver Lining in China’s Cloud Market, Bain & Company, July 2015 [↩]