Dr Pepper Earnings Review: Strong Organic Growth Across Sparkling And Non-Sparkling Segments

As expected, Dr Pepper Snapple (NYSE:DPS) reported a solid set of Q3 results on October 22. [1] The company’s non-carbonated profile led growth with a 4% rise in volume sales, but the carbonated soft drinks (CSD) lineup also contributed to the strong results, witnessing a 2% year-over-year rise in volumes this quarter. CSDs form approximately 80% of all Dr Pepper’s volume sales, and considering that the U.S. accounts for ~90% of the net sales for the beverage manufacturer, performance of Dr Pepper in the U.S. CSDs is crucial to our analysis. But apart from U.S. CSDs, we will talk about the growth in non-sparkling volumes, particularly in Dr Pepper’s allied brands.

See Our Complete Analysis For Dr Pepper Snapple

Dr Pepper’s CSD Portfolio Is Where The Company Wants It To Be

Currency neutral organic sales for the quarter rose 5% year-over-year in Q3 and year-to-date, on a 3% increase in sales volumes, and 3 percentage points of favorable product and package mix and price increases. Dr Pepper expects combined price and mix to be up around 3% for the full year, of which concentrate pricing is expected to drive about 40 basis points of the increase. But there is more room for Dr Pepper to grow in terms of pricing. The company’s price mix is still lower than that of Coca-Cola and PepsiCo, both of which have gained from the introduction of several smaller packages, which have higher prices per unit. A very small percentage of Dr Pepper’s bottle can volume in the U.S. is in the small cans, such as the 8 ounce and 8.5 ounce packs. The customer is moving in the direction of small bottles and cans, which contain lower cumulative calories, and so is the company. Dr Pepper might be late to arrive at the party, but if and when it does, it will have more room to grow. And considering that the company is already growing by more than its almost-omnipresent competitors, this puts the company in a good position.

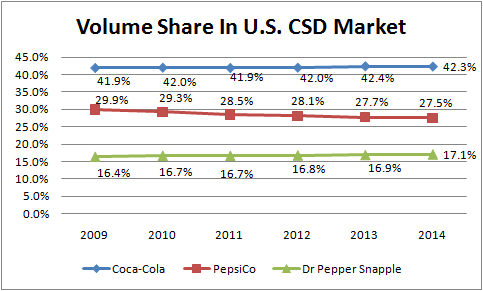

Apart from pricing, Dr Pepper’s volume growth, even for CSDs, has outpaced the industry so far this year. The brand Dr Pepper remained flat in the quarter, with regular Dr Pepper growing 2% and Diet Dr Pepper declining 4%. Both the 2% gain in regular and 4% decline in diet represents better than overall category performance. As consumers continue to cut back on their calorie consumption, the U.S. CSD market has declined for ten consecutive years now. Volume growth in this market is hard to come by, and is made even tougher due to the dominance of Coca-Cola and PepsiCo, which together account for almost 70% of the segment volumes. However, as seen from the chart, Dr Pepper has been able to consistently improve its volume share in an otherwise mature CSD market.

Non-Carbonated Portfolio Spearheads Growth

As customers continue to ditch calorie-fueled sodas, volume sales of other segments such as bottled water, energy drinks, sports drinks, ready-to-drink teas and coffees, etc. have been rising. Seeing customers transition, beverage companies have also had to increase their focus on these other drink categories. While CSD unit sales have grown 2% year-over-year through the first nine months of the year, still beverage volume has grown 4% for Dr Pepper. 20% of Dr Pepper’s volume sales are constituted by still beverages, but this segment is the one presenting the most growth opportunities.

The company has strong non-carbonated brands such as the Snapple tea brand, which has grown by 7% year-to-date. In fact, as the company is focusing on the premium line of its Snapple tea brand, the effective net pricing and margins are getting a boost. The water category rose an impressive 16% in Q3, primarily on growth in FIJI and Bai 5, which the company distributes. Growth in allied brands which have distribution agreements with Dr Pepper bodes well for the company’s future. The allied brands growth is included in the packaged beverage volumes for Dr Pepper, which is the distribution wing for these small but fast growing brands such as Bai 5, Vita Coco, etc. At the gross margin line, the allied brands tend to carry lower gross margin because they have somebody else’s manufacturing profit in there, but are good contributors to Dr Pepper’s operating profitability. Allied brands form a small proportion of net volumes at present, but are an important factor of growth.

What bodes well for Dr Pepper, in comparison to its chief rivals Coca-Cola and PepsiCo, is that the company’s strong organic growth gets realized into revenues. While markets outside the U.S. form approximately 55% and 50% of the net sales for Coca-Cola and PepsiCo, respectively, only 12% of Dr Pepper’s top line is formed by international markets. (In 2014, 4% and 8% of the net sales came from Canada, and from Mexico and the Caribbean, respectively). While currency was a 8% and 12% headwind for Coca-Cola and PepsiCo’s Q3 sales respectively, it was only a 2% headwind for Dr Pepper, allowing net sales to grow positively (3% in the quarter and year-to-date). The domestic market has been kind to Dr Pepper, which is expected to grow by more than the anticipated growth for both Coca-Cola and PepsiCo in the U.S. through the end of the year.

See the links below for more information and analysis:

- Dr Pepper Snapple pre-earnings: domestic market dependence a positive

- Coca-Cola earnings review: another quarter where growth gets wiped out by currency translations

- PepsiCo earnings review: core performance remains strong, although marred by structural changes

- Bottled water is a potential growth category that can’t be ignored

- Soda makers wonder: where could growth in U.S. come from?

- The strong dollar is weighing down these large beverage companies

- Trefis analysis: Dr Pepper North America CSD Revenues

- Trefis analysis: PepsiCo Soft Drink Revenues

- Trefis analysis: Coca-Cola Revenues

View Interactive Institutional Research (Powered by Trefis):

Global Large Cap | U.S. Mid & Small Cap | European Large & Mid Cap

More Trefis Research